A telecom carrier and a retailer are showing a mirror to India’s tryst with assisted corporate demise and rebirth. The image staring back is one of defeat snatched from the jaws of victory. As the five-year-old bankruptcy experiment flounders, blame it on what development scholars refer to as “isomorphic mimicry<\/a>”: Emerging economies ape the form of successful Western institutions but leave them dysfunctional and devoid of content, almost guaranteeing their failure.

Global investors were genuinely excited by India’s 2016 insolvency law, hoping to profit from Rs 19 lakh crore ($260 billion) of bad loans, including those written off by banks in the last eight years. Initial success in finding new homes for distressed steel plants raised hopes that the savings-starved economy would extricate valuable capital from failed ventures. But now, creditors are balking at 90% haircuts, and bailout funds are disillusioned with everything from long delays in admitting cases by tribunals to a chronic shortage of judges.

Large, indebted businesses continue to turn into zombies. Absent a miracle, Vodafone Idea Ltd.<\/a> can’t possibly repay the $30 billion the unprofitable wireless firm owes the government and banks. Future Retail Ltd. was hoping to stay afloat by selling assets to Mukesh Ambani’s bigger empire. But Amazon.com Inc., from which Future’s founder Kishore Biyani had taken money after promising to not sell out to India’s richest man, has legally blocked the deal. Unless Biyani and Amazon can strike a compromise, the pandemic-battered firm’s survival looks iffy.

Corporate death is a feature of capitalism, not a bug. India copied the British playbook of putting creditors in charge of insolvent firms. Debtors can initiate in-court bankruptcy proceedings, or lenders can pull the plug. On paper, everything looks fine. But if the institution was actually working to its intended purpose, India Inc. wouldn’t still be grappling with large enterprises that are both living and dead — just like the fabled cat in quantum physicist Erwin Schrödinger's thought experiment.

There’s no easy answer to what’s gone wrong. As BloombergQuint says, Vodafone Idea<\/a> is reluctant to file. The experience of other bankrupt phone networks doesn’t inspire confidence that it will be allowed to retain its licenses in insolvency. Without them, the carrier with 255 million subscribers is worth very little. Having recently extended the maturity of Future’s $1.4 billion of onshore debt, banks are wary of the loan-loss provisions they’ll have to make by dragging it to a bankruptcy tribunal. It’s a Catch-22: Recoveries could be dismal later. Last week, Future paid the coupon on its offshore bonds within the 30-day grace period. However, the notes are still trading at about 60 cents to the dollar.

No two bankruptcies are the same, but India’s processes for handling them have some common deficiencies. Across the country, 27 tribunals are being run by 29 judges; at least 25 short of what’s required. Many have no experience in financial matters. One judge, M.B. Gosavi, sits on four benches. Cases from Noida, a suburb of Delhi where big builders have defaulted to homebuyers, land before a single tribunal member 300 miles away. The insolvency courts also adjudicate unrelated matters under the Companies Act, overwhelming an already strained system.

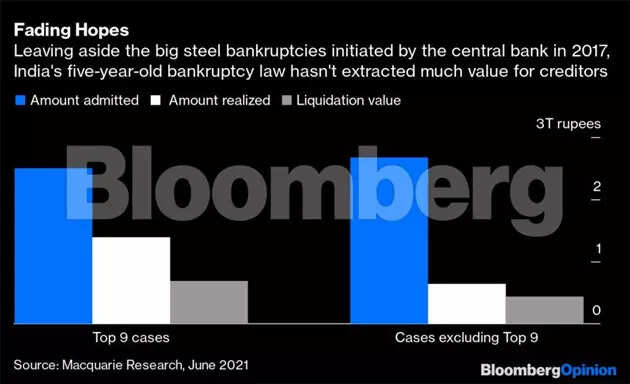

Fading hopes

<\/strong>

Delays abound, not just in approving a sale or liquidation in 270 days as the law proposed originally (the time limit was later increased to 330 days), but even in admitting cases to start the clock. Punjab National Bank<\/a> has tried in vain since November 2018 to put Indian Steel Corp. into bankruptcy. KKR & Co.’s India unit moved against Sintex-BAPL Ltd. a year ago. But an operational creditor came up with its own petition against the auto parts maker, settled with it, and the firm exited bankruptcy. KKR’s application was finally admitted only last month. Leaving aside the top nine bankruptcies initiated in 2017 at the central bank’s behest, creditors’ recovery rate has been just 24%, according to Macquarie Research<\/a>.

The current corporate landscape is a colonial legacy. A handful of British managing agencies used to hold sway over large swathes of productive assets with very little capital. The agencies, which came to be controlled by Indian business families, were outlawed in 1969, but a heavily state-dominated banking system still allows empire-building by politically connected debtors on a sliver of loss-absorbing equity. When government-owned banks lose money, taxpayers fill the hole.

The power imbalance and the perverse incentives were known when parliament legislated the bankruptcy law<\/a>. So lawmakers packed it with creditor-friendly features. But then came the inevitable pushback. Politicians, who have to contest expensive elections with corporate donations, simply lost their nerve for tough love. Urjit Patel, the previous central bank governor who sought to make large borrowers more accountable by ending banks’ evergreening of soured loans, failed and quit abruptly.

It’s still not too late to turn the bankruptcy regime into a real institution. Maybe it will happen only once the state is no longer a dominant player in the lending market. But even awaiting bank privatisation, procedural infirmities can be fixed relatively easily if politicians want to put a stop to misallocation of capital. Perhaps they don’t. As economist Lant Pritchett and others have noted, isomorphic mimicry<\/a> is a great technique for ensuring persistent, successful failure.

<\/body>","next_sibling":[{"msid":85551339,"title":"Nokia shipped nearly 12.8 mn handsets in Q2","entity_type":"ARTICLE","link":"\/news\/nokia-shipped-nearly-12-8-mn-handsets-in-q2\/85551339","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[{"msid":"85552081","title":"View: India is no country for dying companies","entity_type":"IMAGES","seopath":"news\/company\/corporate-trends\/view-india-is-no-country-for-dying-companies","category_name":"View: India is no country for dying companies","synopsis":"There\u2019s no easy answer to what\u2019s gone wrong.","thumb":"https:\/\/etimg.etb2bimg.com\/thumb\/img-size-40240\/85552081.cms?width=150&height=112","link":"\/image\/company\/corporate-trends\/view-india-is-no-country-for-dying-companies\/85552081"}],"msid":85552102,"entity_type":"ARTICLE","title":"View: India is no country for dying companies","synopsis":"Initial success in finding new homes for distressed steel plants raised hopes that the savings-starved economy would extricate valuable capital from failed ventures. But now, creditors are balking at 90% haircuts, and bailout funds are disillusioned with everything from long delays in admitting cases by tribunals to a chronic shortage of judges.","titleseo":"telecomnews\/view-india-is-no-country-for-dying-companies","status":"ACTIVE","authors":[],"analytics":{"comments":0,"views":5150,"shares":0,"engagementtimems":12328000},"Alttitle":{"minfo":""},"artag":"Bloomberg","artdate":"2021-08-23 08:42:19","lastupd":"2021-08-23 08:43:21","breadcrumbTags":["Vodafone Idea","isomorphic mimicry","ibc","bankruptcy code","insolvency cases","bankruptcy law","vodafone idea ltd.","macquarie research","punjab national bank","Industry"],"secinfo":{"seolocation":"telecomnews\/view-india-is-no-country-for-dying-companies"}}" data-authors="[" "]" data-category-name="" data-category_id="" data-date="2021-08-23" data-index="article_1">

- Telecom乐动扑克News

- 4分钟阅读

观点:印度是垂死挣扎的公司没有一个国家

最初的成功为陷入困境的钢铁厂找到新房子带来了希望,savings-starved经济从失败的投资将使宝贵的资本。但是现在,债权人对90%的发型,救助资金对从长延迟在承认情况下通过法庭法官长期短缺。

由安迪•穆克吉

电信运营商和零售商也显示出一面镜子到印度与辅助企业死亡和重生的幽会。盯着回来是一个失败的形象从胜利的下巴。五岁的破产实验由于找不到,要怪就怪发展学者称为“同构模仿”:新兴经济体猿的形式成功的西方金融机构,但让他们混乱和缺乏内容,几乎保证他们的失败。

全球投资者是印度2016年破产法律感到非常兴奋,希望获利19个十万的卢比(合2600亿美元)的不良贷款,包括注销银行在过去的八年。最初的成功为陷入困境的钢铁厂找到新房子带来了希望,savings-starved经济从失败的投资将使宝贵的资本。但是现在,债权人对90%的发型,救助资金对从长延迟在承认情况下通过法庭法官长期短缺。

大,负债累累的企业继续变成僵尸。没有一个奇迹,沃达丰(Vodafone)有限公司。不可能无利可图的无线公司欠偿还300亿美元政府和银行。未来零售有限公司希望通过出售资产来维持下去穆凯什•安巴尼的大帝国。但是Amazon.com Inc .,未来的创始人基肖尔Biyani了钱后承诺不会出售给印度首富,有法律阻止了这一交易。除非Biyani和亚马逊就可以达成妥协,pandemic-battered公司的生存看起来可疑的。

企业死亡是资本主义的特性,而不是bug。印度复制英国剧本负责破产企业的债权人。债务人可以发起在法庭破产程序,或贷款人可以拔掉插头。在纸上,一切都看起来不错。但如果机构实际上是工作目的,印度公司不会仍然是解决大型企业,都是活的和死的——就像传说中的猫在量子物理学家欧文薛定谔的思想实验。

没有简单的答案,出了什么事。正如BloombergQuint所说,沃达丰的想法不愿文件。其他破产的电话网络的经验并不激发信心,它将被允许保留其在破产执照。没有他们,2.55亿用户的载体是值得非常少。最近延长了未来在岸的14亿美元债务到期,银行对贷款损失准备金他们会通过拖拽到破产法庭。“第22条军规”:经济复苏可能是惨淡的。上周,未来在其海外债券息票支付在30天的宽限期。然而,笔记仍然在约60美分美元交易。

破产没有两个是相同的,但是印度的流程来处理一些常见的缺陷。全国27个法庭都由29个法官;至少25短的要求。许多人在金融事务方面没有经验。一个法官,M.B. Gosavi坐在四个长椅。情况下从诺伊达,新德里郊区的大建筑商违约购房者,土地在300英里以外的一个法庭成员。破产法院还裁定不相关问题在公司法下,压倒性的本已紧张的系统。

渺茫的希望

延迟比比皆是,而不仅仅是在270天内批准出售或清算法律最初提出的期限(后来增加到330天),但即使是在承认情况下启动时钟。旁遮普国家银行2018年11月以来已经徒劳无功把印度钢铁公司破产。KKR & Co .)的印度单位对Sintex-BAPL ltd .)一年前。但运营债权人提出自己的反对汽车零部件制造商的请愿书,定居,和该公司退出破产。KKR的申请终于承认上个月。抛开上面九个破产启动2017年在中央银行的要求,债权人回收率仅为24%,据麦格理研究。

当前企业景观是一个殖民遗产。少数英国管理机构用于控制了大片的生产性资产很少的资本。机构,它是由印度商业家庭,在1969年被取缔,但严重国家主导的银行体系仍然允许扩张政治关联的债务人在吸收亏损的股本总额的一小部分。当国有银行亏损,纳税人填补这个洞。

权力失衡和不正当的动机在议会立法破产法。所以议员包装creditor-friendly特性。但随后不可避免的阻力。政治家,曾参加昂贵的选举与企业捐赠,只是为严厉的爱失去了他们的神经。Urjit Patel,前央行行长为了使大型借款人更负责任,结束了银行的不良贷款的不断更新,突然失败,退出。

还不太晚将破产制度变成一个真正的机构。也许只会发生一次国家不再是一个贷款市场的主导者。但即使等待银行私有化,程序性软弱可以固定相对容易,如果政客们想制止资本分配不当。也许他们不喜欢。正如经济学家学院Lant Pritchett和其他人所注意到的那样,同构模仿是一个伟大的技术,以确保持续的、成功的失败。

电信运营商和零售商也显示出一面镜子到印度与辅助企业死亡和重生的幽会。盯着回来是一个失败的形象从胜利的下巴。五岁的破产实验由于找不到,要怪就怪发展学者称为“同构模仿”:新兴经济体猿的形式成功的西方金融机构,但让他们混乱和缺乏内容,几乎保证他们的失败。

全球投资者是印度2016年破产法律感到非常兴奋,希望获利19个十万的卢比(合2600亿美元)的不良贷款,包括注销银行在过去的八年。最初的成功为陷入困境的钢铁厂找到新房子带来了希望,savings-starved经济从失败的投资将使宝贵的资本。但是现在,债权人对90%的发型,救助资金对从长延迟在承认情况下通过法庭法官长期短缺。

大,负债累累的企业继续变成僵尸。没有一个奇迹,沃达丰(Vodafone)有限公司。不可能无利可图的无线公司欠偿还300亿美元政府和银行。未来零售有限公司希望通过出售资产来维持下去穆凯什•安巴尼的大帝国。但是Amazon.com Inc .,未来的创始人基肖尔Biyani了钱后承诺不会出售给印度首富,有法律阻止了这一交易。除非Biyani和亚马逊就可以达成妥协,pandemic-battered公司的生存看起来可疑的。

企业死亡是资本主义的特性,而不是bug。印度复制英国剧本负责破产企业的债权人。债务人可以发起在法庭破产程序,或贷款人可以拔掉插头。在纸上,一切都看起来不错。但如果机构实际上是工作目的,印度公司不会仍然是解决大型企业,都是活的和死的——就像传说中的猫在量子物理学家欧文薛定谔的思想实验。

没有简单的答案,出了什么事。正如BloombergQuint所说,沃达丰的想法不愿文件。其他破产的电话网络的经验并不激发信心,它将被允许保留其在破产执照。没有他们,2.55亿用户的载体是值得非常少。最近延长了未来在岸的14亿美元债务到期,银行对贷款损失准备金他们会通过拖拽到破产法庭。“第22条军规”:经济复苏可能是惨淡的。上周,未来在其海外债券息票支付在30天的宽限期。然而,笔记仍然在约60美分美元交易。

破产没有两个是相同的,但是印度的流程来处理一些常见的缺陷。全国27个法庭都由29个法官;至少25短的要求。许多人在金融事务方面没有经验。一个法官,M.B. Gosavi坐在四个长椅。情况下从诺伊达,新德里郊区的大建筑商违约购房者,土地在300英里以外的一个法庭成员。破产法院还裁定不相关问题在公司法下,压倒性的本已紧张的系统。

渺茫的希望

延迟比比皆是,而不仅仅是在270天内批准出售或清算法律最初提出的期限(后来增加到330天),但即使是在承认情况下启动时钟。旁遮普国家银行2018年11月以来已经徒劳无功把印度钢铁公司破产。KKR & Co .)的印度单位对Sintex-BAPL ltd .)一年前。但运营债权人提出自己的反对汽车零部件制造商的请愿书,定居,和该公司退出破产。KKR的申请终于承认上个月。抛开上面九个破产启动2017年在中央银行的要求,债权人回收率仅为24%,据麦格理研究。

当前企业景观是一个殖民遗产。少数英国管理机构用于控制了大片的生产性资产很少的资本。机构,它是由印度商业家庭,在1969年被取缔,但严重国家主导的银行体系仍然允许扩张政治关联的债务人在吸收亏损的股本总额的一小部分。当国有银行亏损,纳税人填补这个洞。

权力失衡和不正当的动机在议会立法破产法。所以议员包装creditor-friendly特性。但随后不可避免的阻力。政治家,曾参加昂贵的选举与企业捐赠,只是为严厉的爱失去了他们的神经。Urjit Patel,前央行行长为了使大型借款人更负责任,结束了银行的不良贷款的不断更新,突然失败,退出。

还不太晚将破产制度变成一个真正的机构。也许只会发生一次国家不再是一个贷款市场的主导者。但即使等待银行私有化,程序性软弱可以固定相对容易,如果政客们想制止资本分配不当。也许他们不喜欢。正如经济学家学院Lant Pritchett和其他人所注意到的那样,同构模仿是一个伟大的技术,以确保持续的、成功的失败。

评论

现在评论 阅读评论(1)所有评论

找到这个评论进攻?

下面选择你的理由并单击submit按钮。这将提醒我们的版主采取行动