MUMBAI: The Supreme Court<\/a> (SC) on Tuesday ruled that payments<\/a> made by resident Indian end-users or distributors (such as technology companies) to overseas suppliers on import of ‘shrink-wrapped’ software<\/a> – generally known as off-the-shelf software, is not a ‘Royalty’ payment. Thus, no withholding tax obligations arise in India, against such payment. 最高法院(SC)周二裁定,常驻印度最终用户或经销商的付款方式(如科技公司)对进口海外供应商“包装”软件——通常被称为现成的软件,不是一个“皇室”付款。因此,没有代扣所得税义务出现在印度,这样的付款。 孟买:最高法院(SC)周二裁定支付由居民印度最终用户或经销商(如科技公司)海外供应商进口“包装”软件——通常被称为现成的软件,不是一个“皇室”付款。因此,没有代扣所得税义务出现在印度,这样的付款。

During assessment and at various levels of judicial appeals, payments made for import of shrink-wrapped software to overseas suppliers was held assessable to tax as ‘Royalty’ under section 9(1)(vi) of the I-T Act and Article 12 of the respective tax treaties. This classification as ‘Royalty’ required tax to be deducted at source (TDS<\/a>) when making payment to the overseas suppliers.

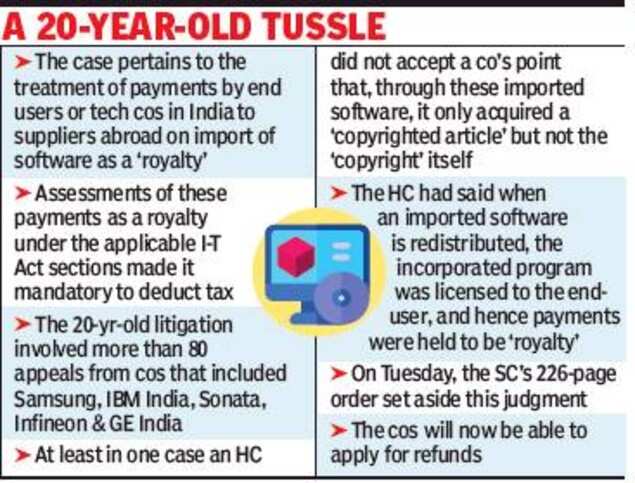

As TDS obligations were not met, the Indian distributors were held to be ‘assessees in default’ – heavy tax demands, which included penalties were raised on them. Now, they will be able to file for refund, which according to industry observers could run into several lakhs.

Over several days in February, the apex court heard a batch of more than 80 appeals, covering this issue of ‘Royalty’ payment. The companies involved in this prolonged litigation that lasted nearly twenty years, included Samsung Electronics<\/a>, IBM India<\/a>, Sonata Information Technology, Infineon Technologies<\/a>, GE India Technology Centre, to name a few.

In short, the contention of the companies was that the use of software by the Indian importer was limited to making a backup copy and\/or redistribution. They did not have the right to modify the shrink-wrapped software that was imported.

So, the payment made to the overseas supplier could not be treated as ‘Royalty’ but could only be treated as business income in the hands of the overseas entity and no tax withholding obligations arose. Today, in an order spanning 226 pages, the Supreme Court had upheld this stand and has set aside high court judgements that had held otherwise.

For instance, in 2011, the Karnataka high court in the case of Samsung Electronics had held that payment made for purchase of shrink-wrapped or off-the-shelf software was in the nature of ‘Royalty’. It had turned down the contention of the company that on purchase of shrink-wrapped software, it only acquired a ‘copyrighted article’ but not the ‘copyright’ itself, hence the amount paid was not assessable as ‘Royalty’.

According to the Karnataka high court, when the software was redistributed the incorporated program was licensed to the end-user, hence the payments were held to be ‘Royalty’. This judgement is now set aside.

Hitesh Gajaria, senior partner at KPMG India<\/a> states, “This welcome judgement puts at rest the widespread litigation on this contentious issue and gives relief to Indian companies who were being pursued by the I-T department for alleged non-withholding of Income-tax on payments made for purchasing computer software from non-residents.”

“Even as a new Equalisation Levy on non-resident e-commerce operators selling goods and services has come into force with mind-bogglingly vast scope and coverage, thankfully here the burden has been cast on those overseas companies to comply with the provisions of this new levy,” adds Gajaria.

Rakesh Nangia, chairman, Nangia Andersen India states, “The apex court today put a happy end to the twenty years old software-royalty tax dispute, by ruling in favour of the taxpayers, stating that cross-border payments made for sale of software to a non-resident is not be taxed as ‘Royalty’. It was a much-awaited order and will put to rest open litigation on this issue.”

Glimpses of submissions before the Supreme Court<\/strong>

The SC heard these batch of appeals for several days in February. It observed that the appeals could be grouped in four categories. The first category deals with cases in which computer software is purchased directly by an end-user, resident in India, from a foreign, non-resident supplier or manufacturer.

The second category of cases deals with resident Indian companies that act as distributors or resellers, by purchasing computer software from foreign, non-resident suppliers or manufacturers and then reselling the same to resident Indian end-users.

The third category concerns cases wherein the distributor happens to be a foreign, non-resident vendor, who, after purchasing software from a foreign, non-resident seller, resells the same to resident Indian distributors or end-users.

The fourth category includes cases wherein computer software is affixed onto hardware and is sold as an integrated unit\/equipment.

The three-judge bench comprising of Justice R F Nariman, Justice Hemant Gupta and Justice B.R. Gavai held, “The amounts paid by resident Indian end-users\/distributors to non-resident computer software manufacturers\/ suppliers, as consideration for the resale\/use of the computer software through EULAs\/distribution agreements, is not the payment of royalty for the use of copyright in the computer software, and that the same does not give rise to any income taxable in India, as a result of which the persons referred to in section 195 of the Income Tax Act were not liable to deduct any TDS under section 195 of the I-T Act. The answer to this question will apply to all four categories of cases enumerated by us…”

The parties that had filed the appeal before the SC were represented by well- known stalwarts. For instance, Arvind Datar, senior advocate who appeared on behalf of IBM India contended that earlier the apex court in the case of TCS had held that packaged software constituted ‘goods’.

IBM India was a non-exclusive distributor of shrink-wrapped computer software. It did not own any right, title or interest in copyright and other intellectual property owned by IBM Singapore, and merely marketed IBM Singapore’s software products in India. It did not pay any consideration for the transfer of or interest in the copyright, thus such payments could not be categorised as ‘Royalty’ was his argument.

S. Ganesh, senior advocate, who appeared on behalf of Sonata Information Technology submitted that the provisions of section 52(1)(aa) of the Copyright Act 1957, gives the buyers of computer programs the right to make a copy if: It is done to utilise the computer program for the purpose for which it was supplied, or it is done to make backup copies for emergencies. The right to make a copy in order to use the software, does not imply that a ‘copyright’ has been assigned.

While the Finance Act, 2012, amended the I-T Act to widen the applicability of the Royalty provisions, most transactions in dispute were covered by the narrower definition provided in tax treaties. However, submissions were also placed that this retrospective amendment cannot apply to the cases being heard by the SC.

Ajay Vohra, senior advocate appearing on behalf of Sasken Communications Tech submitted that the retrospective amendment to section 9(1)(vi) of the I-T Act by adding Explanation 4, could not be applied as the assessment years of the matters being heard by the SC were prior to 2012.

He emphasised that “…the law cannot compel one to do the impossible, namely, to deduct tax at source on an expanded definition of royalty which did not exist at the time of the payment\/deduction to be made under section 195 of the I-T Act.”

<\/p><\/body>","next_sibling":[{"msid":81303494,"title":"U.S. ITC to probe some cellular devices made by Samsung, Motorola Mobility","entity_type":"ARTICLE","link":"\/news\/u-s-itc-to-probe-some-cellular-devices-made-by-samsung-motorola-mobility\/81303494","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[{"msid":"81297046","title":"Supreme Court","entity_type":"IMAGES","seopath":"business\/india-business\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court\/supreme-court","category_name":"No TDS required on import of shrink-wrapped software: Supreme Court","synopsis":false,"thumb":"https:\/\/etimg.etb2bimg.com\/thumb\/img-size-106126\/81297046.cms?width=150&height=112","link":"\/image\/business\/india-business\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court\/supreme-court\/81297046"}],"seoschemas":false,"msid":81303538,"entity_type":"ARTICLE","title":"No TDS required on import of shrink-wrapped software: Supreme Court","synopsis":"The Supreme Court (SC) on Tuesday ruled that payments made by resident Indian end-users or distributors (such as technology companies) to overseas suppliers on import of \u2018shrink-wrapped\u2019 software \u2013 generally known as off-the-shelf software, is not a \u2018Royalty\u2019 payment. Thus, no withholding tax obligations arise in India, against such payment.","titleseo":"telecomnews\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court","status":"ACTIVE","authors":[{"author_name":"Lubna Kably","author_link":"\/author\/4757\/lubna-kably","author_image":"https:\/\/etimg.etb2bimg.com\/authorthumb\/4757.cms?width=250&height=250&imgsize=7655","author_additional":{"thumbsize":true,"msid":4757,"author_name":"Lubna Kably","author_seo_name":"Lubna-Kably","designation":"Senior Editor","agency":false}}],"Alttitle":{"minfo":""},"artag":"TNN","artdate":"2021-03-03 08:13:59","lastupd":"2021-03-03 08:14:44","breadcrumbTags":["Supreme Court","Samsung Electronics","TDS","software","payments","Infineon Technologies","IBM India","KPMG India","policy"],"secinfo":{"seolocation":"telecomnews\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court"}}" data-authors="[" lubna kably"]" data-category-name="" data-category_id="" data-date="2021-03-03" data-index="article_1">

不需要TDS进口的包装软件:最高法院

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

评估和各级司法上诉期间,支付进口包装软件的海外供应商应评税税收是“皇室”举行下一节9 (1)(vi)它的行动和第十二条各自的税收条约。这种分类为“皇室”需要在源(扣除税收TDS当海外供应商付款。

TDS义务并不满足,印度经销商被认为是“阿塞斯违约”——重税的要求,提出了包括处罚。现在,他们可以申请退款,据业内观察人士可能遇到几个卢比。

在2月份的几天,先端上诉法院,听到一批80多覆盖“皇室”付款的这个问题。这漫长的诉讼所涉及的公司持续了将近二十年,包括在内三星电子,IBM印度奏鸣曲信息技术,英飞凌科技通用电气印度技术中心,等等。

简而言之,企业的竞争由印度进口商使用软件仅限于做一个备份拷贝和/或重新分配。他们没有权利修改包装进口的软件。

所以,海外供应商的付款不能被视为皇室,但只能作为营业收入的海外实体和没有扣缴义务出现。今天,在订单生成226页,最高法院支持这个站,并留出高等法院判断,否则举行。

例如,2011年,卡纳塔克邦最高法院在三星电子的情况下举行,付款购买的包装或现成的软件是在“皇室”的本质。它拒绝了公司的竞争,在购买的软件,它只获得了受版权保护的文章,但不是“版权”本身,因此,支出金额不应评税“皇室”。

根据卡纳塔克邦最高法院,当软件重新整合项目授权给最终用户,因此支付举行“皇室”。这种判断现在备用。

语Gajaria,高级合伙人毕马威(KPMG)印度州,“这欢迎判断静止了广泛的诉讼在这个有争议的问题和舒缓印度公司被它部门追求所谓non-withholding所得税的支付从非居民购买计算机软件。”

“即使对非居民征收新的平衡电子商务运营商出售产品和服务生效了令人难以置信的巨大范围和覆盖面,幸好这里的负担已经投在那些海外公司遵守这个新税的规定,“Gajaria补充道。

主席拉克什Nangia Nangia安徒生印度国家,“法院今天将结束二十岁快乐software-royalty税务纠纷,有利于纳税人的判决,说明跨境支付非居民出售的软件不是被视作“皇室”征税。这是一个期待已久的秩序,将休息在这个问题上公开诉讼。”

之前提交的最高法院

SC听到这些批2月份上诉好几天。它观察到上诉可以分为四类。第一类处理情况下,计算机软件是由一个终端用户直接购买,居民在印度,从外国,非居民供应商或制造商。

第二类情况下处理居民印度公司作为分销商或零售商,,非居民通过购买计算机软件从外国供应商或制造商,然后转售相同的居民印度最终用户。

第三类问题情况下,经销商是外国,非居民厂商,从外国购买软件后,非居民的卖家,出售相同的常驻印度经销商或最终用户。

第四类包括病例在计算机软件上到硬件和销售作为一个集成单元/设备。

由三名法官组成的长椅上由司法部R F纳里曼,正义赫曼特古普塔和正义开国元勋之一B.R.安贝德卡对Gavai举行,“印度居民支付的金额最终用户/经销商非居民计算机软件制造商/供应商,考虑转售/使用的计算机软件通过eula /分销协议,不支付版税的使用计算机软件著作权,同样,不产生任何收入应税在印度,结果的人称为section 195的所得税法没有责任扣除任何TDS section 195的它行动。这个问题的答案将适用于所有我们所列举的四类案件中…”

当事人提起上诉的SC是由前——已知的中坚分子。例如,Arvind塔尔、高级提倡出现代表IBM印度法院的早些时候声称TCS举行了,打包的软件构成了“商品”。

IBM印度是一个非排他性经销商用收缩膜包装的计算机软件。它没有自己的任何权利,标题或兴趣版权和其他知识产权属于IBM新加坡、新加坡和仅仅销售IBM在印度的软件产品。它没有支付任何考虑版权的转让或兴趣,因此此类支付不能归类为“皇室”是他的论点。

s . Ganesh高级提倡在代表奏鸣曲信息技术提交的规定部分52 (1)(aa)的版权法案1957年,给了买家的计算机程序复制的权利如果:它是利用计算机程序的目的是提供,或是让紧急备份副本。复制权为了使用软件,并不意味着已经指定了一个“版权”。

财政法案,2012年修改了它采取行动扩大版税条款的适用性,大多数交易纠纷都由狭义的定义中提供税收条约。然而,提交也放在这回顾修正案不能适用于SC的情况下被听到。

Ajay Vohra高级代表Sasken提倡出现通讯科技提交回顾性修正案部分9 (1)(vi)它法案的通过添加解释4,无法应用的评估年听到的事情SC 2012年之前。

他强调“…法律不能强迫做不可能的事,也就是说,扣除税收在皇室的扩展定义源不存在时的付款/扣除这法案195条款下了。”

MUMBAI: The Supreme Court<\/a> (SC) on Tuesday ruled that payments<\/a> made by resident Indian end-users or distributors (such as technology companies) to overseas suppliers on import of ‘shrink-wrapped’ software<\/a> – generally known as off-the-shelf software, is not a ‘Royalty’ payment. Thus, no withholding tax obligations arise in India, against such payment.

During assessment and at various levels of judicial appeals, payments made for import of shrink-wrapped software to overseas suppliers was held assessable to tax as ‘Royalty’ under section 9(1)(vi) of the I-T Act and Article 12 of the respective tax treaties. This classification as ‘Royalty’ required tax to be deducted at source (TDS<\/a>) when making payment to the overseas suppliers.

As TDS obligations were not met, the Indian distributors were held to be ‘assessees in default’ – heavy tax demands, which included penalties were raised on them. Now, they will be able to file for refund, which according to industry observers could run into several lakhs.

Over several days in February, the apex court heard a batch of more than 80 appeals, covering this issue of ‘Royalty’ payment. The companies involved in this prolonged litigation that lasted nearly twenty years, included Samsung Electronics<\/a>, IBM India<\/a>, Sonata Information Technology, Infineon Technologies<\/a>, GE India Technology Centre, to name a few.

In short, the contention of the companies was that the use of software by the Indian importer was limited to making a backup copy and\/or redistribution. They did not have the right to modify the shrink-wrapped software that was imported.

So, the payment made to the overseas supplier could not be treated as ‘Royalty’ but could only be treated as business income in the hands of the overseas entity and no tax withholding obligations arose. Today, in an order spanning 226 pages, the Supreme Court had upheld this stand and has set aside high court judgements that had held otherwise.

For instance, in 2011, the Karnataka high court in the case of Samsung Electronics had held that payment made for purchase of shrink-wrapped or off-the-shelf software was in the nature of ‘Royalty’. It had turned down the contention of the company that on purchase of shrink-wrapped software, it only acquired a ‘copyrighted article’ but not the ‘copyright’ itself, hence the amount paid was not assessable as ‘Royalty’.

According to the Karnataka high court, when the software was redistributed the incorporated program was licensed to the end-user, hence the payments were held to be ‘Royalty’. This judgement is now set aside.

Hitesh Gajaria, senior partner at KPMG India<\/a> states, “This welcome judgement puts at rest the widespread litigation on this contentious issue and gives relief to Indian companies who were being pursued by the I-T department for alleged non-withholding of Income-tax on payments made for purchasing computer software from non-residents.”

“Even as a new Equalisation Levy on non-resident e-commerce operators selling goods and services has come into force with mind-bogglingly vast scope and coverage, thankfully here the burden has been cast on those overseas companies to comply with the provisions of this new levy,” adds Gajaria.

Rakesh Nangia, chairman, Nangia Andersen India states, “The apex court today put a happy end to the twenty years old software-royalty tax dispute, by ruling in favour of the taxpayers, stating that cross-border payments made for sale of software to a non-resident is not be taxed as ‘Royalty’. It was a much-awaited order and will put to rest open litigation on this issue.”

Glimpses of submissions before the Supreme Court<\/strong>

The SC heard these batch of appeals for several days in February. It observed that the appeals could be grouped in four categories. The first category deals with cases in which computer software is purchased directly by an end-user, resident in India, from a foreign, non-resident supplier or manufacturer.

The second category of cases deals with resident Indian companies that act as distributors or resellers, by purchasing computer software from foreign, non-resident suppliers or manufacturers and then reselling the same to resident Indian end-users.

The third category concerns cases wherein the distributor happens to be a foreign, non-resident vendor, who, after purchasing software from a foreign, non-resident seller, resells the same to resident Indian distributors or end-users.

The fourth category includes cases wherein computer software is affixed onto hardware and is sold as an integrated unit\/equipment.

The three-judge bench comprising of Justice R F Nariman, Justice Hemant Gupta and Justice B.R. Gavai held, “The amounts paid by resident Indian end-users\/distributors to non-resident computer software manufacturers\/ suppliers, as consideration for the resale\/use of the computer software through EULAs\/distribution agreements, is not the payment of royalty for the use of copyright in the computer software, and that the same does not give rise to any income taxable in India, as a result of which the persons referred to in section 195 of the Income Tax Act were not liable to deduct any TDS under section 195 of the I-T Act. The answer to this question will apply to all four categories of cases enumerated by us…”

The parties that had filed the appeal before the SC were represented by well- known stalwarts. For instance, Arvind Datar, senior advocate who appeared on behalf of IBM India contended that earlier the apex court in the case of TCS had held that packaged software constituted ‘goods’.

IBM India was a non-exclusive distributor of shrink-wrapped computer software. It did not own any right, title or interest in copyright and other intellectual property owned by IBM Singapore, and merely marketed IBM Singapore’s software products in India. It did not pay any consideration for the transfer of or interest in the copyright, thus such payments could not be categorised as ‘Royalty’ was his argument.

S. Ganesh, senior advocate, who appeared on behalf of Sonata Information Technology submitted that the provisions of section 52(1)(aa) of the Copyright Act 1957, gives the buyers of computer programs the right to make a copy if: It is done to utilise the computer program for the purpose for which it was supplied, or it is done to make backup copies for emergencies. The right to make a copy in order to use the software, does not imply that a ‘copyright’ has been assigned.

While the Finance Act, 2012, amended the I-T Act to widen the applicability of the Royalty provisions, most transactions in dispute were covered by the narrower definition provided in tax treaties. However, submissions were also placed that this retrospective amendment cannot apply to the cases being heard by the SC.

Ajay Vohra, senior advocate appearing on behalf of Sasken Communications Tech submitted that the retrospective amendment to section 9(1)(vi) of the I-T Act by adding Explanation 4, could not be applied as the assessment years of the matters being heard by the SC were prior to 2012.

He emphasised that “…the law cannot compel one to do the impossible, namely, to deduct tax at source on an expanded definition of royalty which did not exist at the time of the payment\/deduction to be made under section 195 of the I-T Act.”

<\/p><\/body>","next_sibling":[{"msid":81303494,"title":"U.S. ITC to probe some cellular devices made by Samsung, Motorola Mobility","entity_type":"ARTICLE","link":"\/news\/u-s-itc-to-probe-some-cellular-devices-made-by-samsung-motorola-mobility\/81303494","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[{"msid":"81297046","title":"Supreme Court","entity_type":"IMAGES","seopath":"business\/india-business\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court\/supreme-court","category_name":"No TDS required on import of shrink-wrapped software: Supreme Court","synopsis":false,"thumb":"https:\/\/etimg.etb2bimg.com\/thumb\/img-size-106126\/81297046.cms?width=150&height=112","link":"\/image\/business\/india-business\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court\/supreme-court\/81297046"}],"seoschemas":false,"msid":81303538,"entity_type":"ARTICLE","title":"No TDS required on import of shrink-wrapped software: Supreme Court","synopsis":"The Supreme Court (SC) on Tuesday ruled that payments made by resident Indian end-users or distributors (such as technology companies) to overseas suppliers on import of \u2018shrink-wrapped\u2019 software \u2013 generally known as off-the-shelf software, is not a \u2018Royalty\u2019 payment. Thus, no withholding tax obligations arise in India, against such payment.","titleseo":"telecomnews\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court","status":"ACTIVE","authors":[{"author_name":"Lubna Kably","author_link":"\/author\/4757\/lubna-kably","author_image":"https:\/\/etimg.etb2bimg.com\/authorthumb\/4757.cms?width=250&height=250&imgsize=7655","author_additional":{"thumbsize":true,"msid":4757,"author_name":"Lubna Kably","author_seo_name":"Lubna-Kably","designation":"Senior Editor","agency":false}}],"Alttitle":{"minfo":""},"artag":"TNN","artdate":"2021-03-03 08:13:59","lastupd":"2021-03-03 08:14:44","breadcrumbTags":["Supreme Court","Samsung Electronics","TDS","software","payments","Infineon Technologies","IBM India","KPMG India","policy"],"secinfo":{"seolocation":"telecomnews\/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court"}}" data-news_link="//www.iser-br.com/news/no-tds-required-on-import-of-shrink-wrapped-software-supreme-court/81303538">

评论

现在评论 阅读评论(1)所有评论

找到这个评论进攻?

下面选择你的理由并单击submit按钮。这将提醒我们的版主采取行动